Do investors know what will make them happy?

Yeah, kind of.

My personal views only, not those of my employer, government, family, or dog. The title is meant to be ironic.

Yeah, kind of.

A new paper gives strong indication that on average, individual investors are really poor investors. I mean, really bad.

One of the most provocative questions is what causes some people to end up with lots of money, and some with very little.

Regrets are all about high expectations.

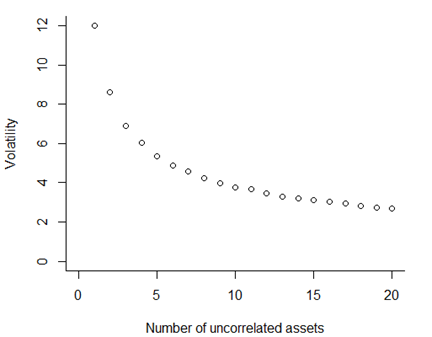

Diversification is always good. It’s just limited in how much good it can do.

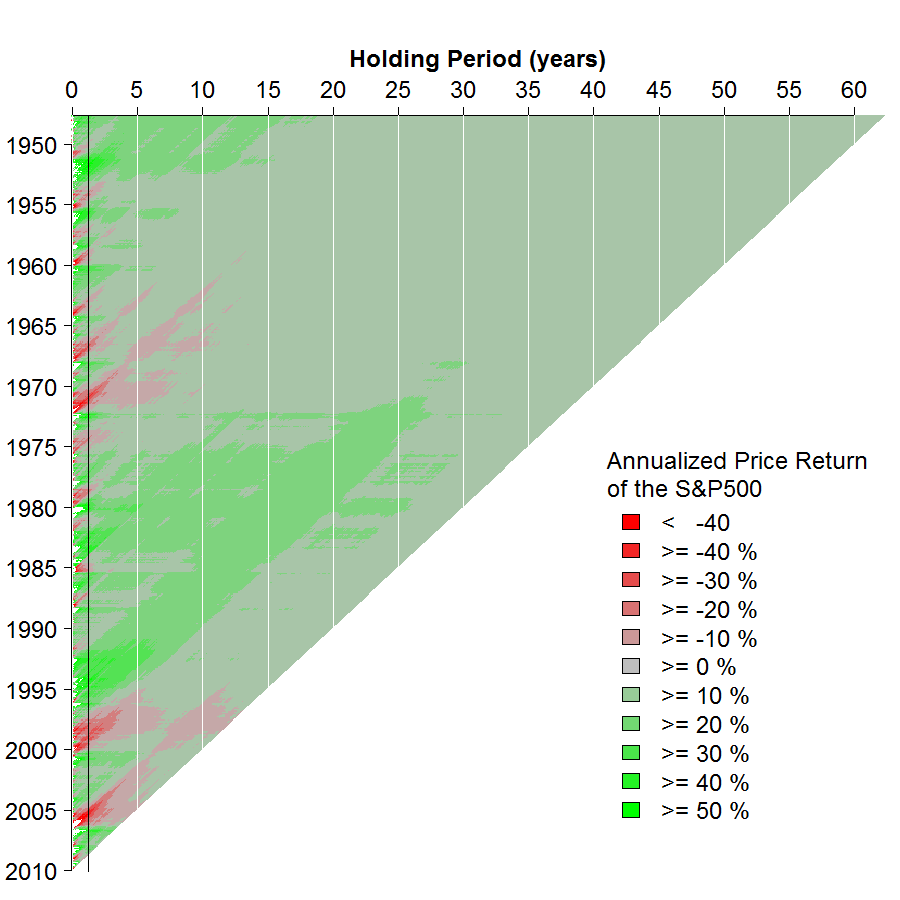

A while ago the great graphics gurus (sorry) at the NYTimes created a very cool graphic showing the annualized returns of the S&P500 over a long time period: This was one of the best graphics I’d seen in a while, but there are a number of things I thought could be improved, or used to illustrate another point. Red doesn’t mean loss. The light red in the picture means a return slightly above inflation.

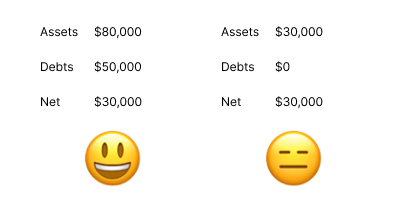

I had the pleasure of meeting up with Abby Sussman of Princeton last night, who investigates the psychology of wealth - assets and liabilities. Her recent piece in Psychological Science sums it up well: We studied the perception of wealth as a function of varying levels of assets and debt. We found that with total gross wealth held constant, people with positive net worth feel and are seen as wealthier when they have lower debt (despite having fewer assets).

I believe unexpected utility is one of the most under-researched ideas in behavioral finance and economics. I, for one, experience it occasionally, and it is the best kind of utility. Photo by Richard Horvath. What, exactly is “unexpected utility”? It’s an experience, usually and hopefully positive, that you completely didn’t remotely see coming. The expectation is key here. Daniel Kahneman, in his recent book, uses the example that the same meal, when made by someone else, often tastes better.

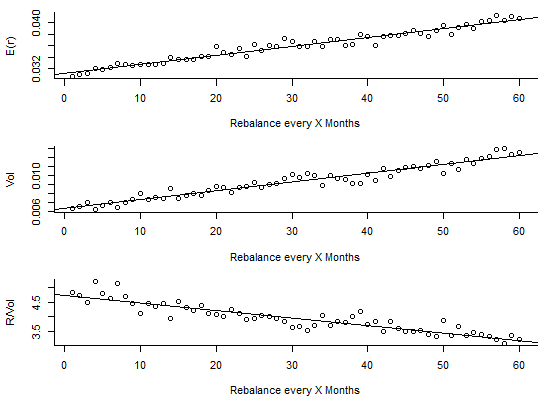

Once we have picked an asset allocation model, how often, or why should we rebalance? I’ve seen multiple conflicting findings about the usefulness of rebalancing. Many such conflicts happen in time-series data because the sample you use can influence things quite strongly. I therefore wanted to see if there was a simple, purely statistical basis for rebalancing. To do this, I simulated some pretty vanilla portfolios with the desired characteristics. Note that as this isn’t real data, it doesn’t have some of the finer characteristics of true returns data such as auto-correlation of volatility.

A problem I occasionally encounter when trying to improve behaviour in the real world is the fairness of control groups. Imagine you have a potential cure for a problem, but you have no proof that it actually works. A standard experiment would randomly allocate individuals to treatment and control conditions, run the experiment for a set period of time, and compare outcome variables. You’d then know if there was a strong effect.