A little bit of confidence is a dangerous thing

May 4, 2017

First comes motivation.

When a person becomes motivated to invest (rather than keep money in a savings account) they want to do a good job. But the learning curve can be steep… and thus expensive. The new investor may pay in time, trading commissions, high expense ratios and of course mental effort. But the price must be paid.

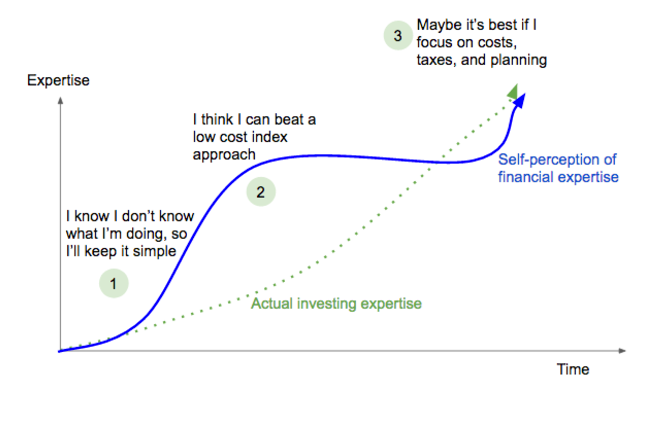

My completely anecdotal, unscientific impression is that a person’s investing expertise follows a path roughly like this:

- At first they know they don’t know, and so avoid it by investing in cash savings accounts.

- As they learn from reading or dipping their toes into trading single name stocks, they get confident. They might branch out into more other macro-speculative asset classes, using levered S&P 500 funds, gold, or commodities. Things they are familiar with. At this point, they are comfortable with trading, listening to the news, feeling like their hand is on the wheel.

- Over time, a very very weak feedback loop kicks in: the single line stocks rip their face off and they can’t sleep at night, they realize for all their trading, they aren’t coming out very far ahead; they realize the commissions are killing them, and decide the pursuit of market alpha isn’t worth it. It generally takes 2 years for 80% of day traders quit trying to beat the market. Some keep losing, but never quit.

- By the end, they often actually are wiser than they think. But more importantly they know how much they don’t know about the future, but do know about things they can control.

As you can see, it’s the ‘little bit of knowledge’ area where the biggest disconnect between perceived expertise and actual expertise occurs. When an investor believes they know about stocks, trading, and they have some ‘system’ that gives them confidence (or fear of losses) to more actively manage their portfolio. That’s where the biggest potential for harm exists, especially if the market has been benevolent so far.

A small, but very common mistake

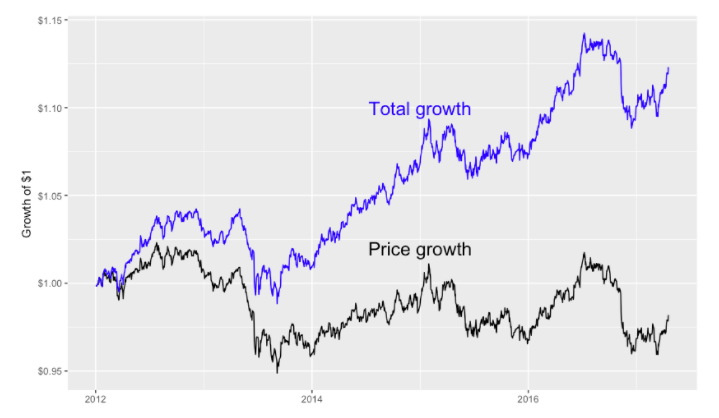

DIY investors often try to make good decisions by consulting free, independent information sources. So if they want to look at the performance of a fund, they might go to finance.yahoo.com, and see this graph of the five year performance of bond fund BND:

This bond fund looks horrible. I mean, granted, the losses haven’t been huge, but there has been no growth over five years. Who would ever invest in that? What a new investor might not realize is that Yahoo Finance graphs display price-only history. For funds which pay out a significant part of their return in coupons or dividends, this systematically under-counts the return. You’re looking at how much it would cost to buy the fund at any point in time, but not how much wealthier you would or wouldn’t be. If you include dividends, BND looks pretty good for a bond fund:

This is a surprisingly common misunderstanding. And it’s just about knowing how to correctly research historical performance, not even about making predictions for the future.

It’s hard to learn well Investing and markets are one of the toughest environments to learn in. An investor doesn’t get high quality feedback they can learn from - sometimes it’s not clear if a decision was good or bad for years, if not decades. It’s hard to assess and compare returns correctly to know if you’d have been better off somewhere else… and that’s a cake walk compared to predicting if you’d be better off investing one way or another.

Easy success and confidence is the enemy If there is one consistent bias in investing, is is overconfidence. Investors trade too much, try to market time to much, and have concentrated portfolios which expose them to significant risk of losing a lot of money. Fortunes are lost much faster than they are made, and while you might get lucky in the short term, you should probably be investing for the right (longish) term. It’s wise to always believe you know a bit less than you should.

Get the education, but don’t pay full private school tuition (If you don’t get the reference, watch Good Will Hunting) To be clear, I’m not saying you shouldn’t experiment, explore and try to figure things out for yourself. Getting your hands dirty and really seeing how things work over a long period of time is a great way to end up a savvy investor. So feel free to make mistakes, just make sure they are mistakes you can afford. When making concentrated bets, only use money you can afford to lose completely. When reacting to market moves, consider making your changes only half as extreme as you might desire. When choosing an active manager, consider it a marriage you’re committing to for at least 7 years, if not longer. Active management is likely to underperform too, and fair-weather active investors have even higher behavior gaps than passive ones.